The terms Income Statement and Profit and Loss (P&L) Statement are often used interchangeably, but are they really the same thing? For many business owners, understanding financial statements is key to managing the financial health of their company, making informed decisions, and reporting accurately to stakeholders. In this blog post, we will explore the differences and similarities between an income statement and a profit and loss statement, how to read and use them, and answer frequently asked questions to help you better understand these crucial financial documents.

What is an Income Statement?

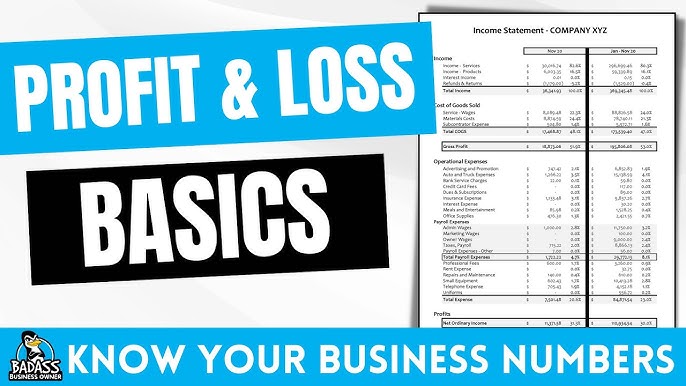

An Income Statement is a financial report that provides a summary of a company’s revenues, expenses, and profits over a specific period, such as a quarter or a year. The primary purpose of an income statement is to show whether the company made a profit or incurred a loss during that period. It is one of the three main financial statements used by businesses, along with the Balance Sheet and Cash Flow Statement.

The income statement is often referred to as the “bottom line” report, as it details how the company’s revenue is transformed into net income.

What is a Profit and Loss (P&L) Statement?

A Profit and Loss Statement, also known as a P&L Statement, is another term commonly used for the income statement. Essentially, both documents serve the same purpose: they outline the revenues, costs, and expenses of a business during a particular period. The P&L statement helps determine whether a company is making a profit or experiencing a loss.

The P&L statement is used by business owners, investors, and analysts to evaluate the financial performance of the company.

Key Components of Income Statement and Profit and Loss Statement

Revenue (Sales): This is the total amount of money earned from the sale of goods or services. It is often referred to as the top line of the statement because it appears at the top of the report.

Cost of Goods Sold (COGS): This is the direct cost associated with producing the goods or services sold by the company. It includes expenses such as raw materials, labor, and manufacturing costs.

Gross Profit: Gross profit is calculated by subtracting COGS from total revenue. It shows how efficiently a company is producing and selling its products.

Operating Expenses: Operating expenses are the day-to-day costs of running the business, such as rent, utilities, salaries, and marketing expenses.

Operating Income: Also known as EBIT (Earnings Before Interest and Taxes), operating income is the profit earned from core business activities after accounting for operating expenses.

Net Income: Net income, also referred to as the bottom line, is the final profit after all expenses, including taxes and interest, have been deducted from revenue.

Income Statement vs Profit and Loss: Is There a Difference?

The terms Income Statement and Profit and Loss Statement are often used interchangeably, and for good reason—they serve the same purpose and contain the same information. The difference between the two terms is largely semantic, as different industries and regions might prefer one term over the other.

In essence:

Income Statement is a formal term commonly used in accounting and financial reporting.

Profit and Loss Statement (P&L) is more colloquial and often used by business owners, particularly in small businesses.

Regardless of the name, both documents are designed to summarize a company’s financial performance over a given period and help stakeholders understand profitability.

How to Use an Income Statement (or P&L Statement)

Analyze Profitability: The main goal of an income statement is to determine whether the company is profitable. By comparing revenues and expenses, you can quickly see if the company is making or losing money.

Identify Trends: Comparing income statements over multiple periods helps identify trends in revenue growth, cost management, and profitability. This information can guide strategic business decisions.

Expense Management: The statement helps you analyze various expense categories, such as operating costs and interest expenses, allowing you to identify areas where the business could reduce costs.

Make Business Decisions: Analyzing the income statement allows business owners to make informed decisions, such as whether to expand, cut costs, or invest in new projects.

Frequently Asked Questions about Income Statements and Profit and Loss Statements

Q1: Are an income statement and a profit and loss statement the same thing?

Yes, the terms income statement and profit and loss statement (P&L) are used interchangeably. Both serve the same purpose of summarizing a company’s revenues, expenses, and net income over a specific period.

Q2: What is the main purpose of an income statement?

The main purpose of an income statement is to provide a summary of the company’s revenues, expenses, and profits or losses during a specific period, helping stakeholders understand the company’s financial performance.

Q3: What is included in an income statement?

An income statement includes revenue, cost of goods sold (COGS), gross profit, operating expenses, operating income, interest and taxes, and net income.

Q4: How often should a business prepare an income statement?

A business should prepare an income statement at least quarterly and annually. Many businesses also prepare monthly income statements to track performance more closely.

Q5: Why is net income called the bottom line?

Net income is called the bottom line because it is the final figure on the income statement that shows the company’s overall profitability after accounting for all expenses.

Q6: How does an income statement differ from a balance sheet?

An income statement shows the company’s financial performance over a specific period, focusing on revenues and expenses, while a balance sheet provides a snapshot of the company’s financial position at a specific point in time, detailing assets, liabilities, and equity.

Q7: Who uses an income statement?

Income statements are used by various stakeholders, including business owners, investors, creditors, and financial analysts, to evaluate a company’s profitability and financial health.

Q8: How can I use an income statement to manage my business?

You can use an income statement to assess profitability, manage expenses, identify trends, and make informed decisions about investments, cost-cutting, or expansion.

Q9: What is gross profit, and how is it calculated?

Gross profit is the profit a company makes after subtracting the cost of goods sold (COGS) from total revenue. It is calculated using the formula:

Q10: Can an income statement show a loss?

Yes, an income statement can show a net loss if the company’s expenses exceed its revenues during the period. This indicates that the company was not profitable.

Conclusion

Whether you refer to it as an income statement or a profit and loss statement (P&L), this financial document is essential for understanding a company’s financial performance. By summarizing revenues, expenses, and profits, the income statement helps stakeholders assess profitability, manage expenses, and make strategic decisions. Understanding the nuances of financial statements like the income statement is key to making informed decisions that drive business success.